Facing Facts: Operator Q3s from across the globe

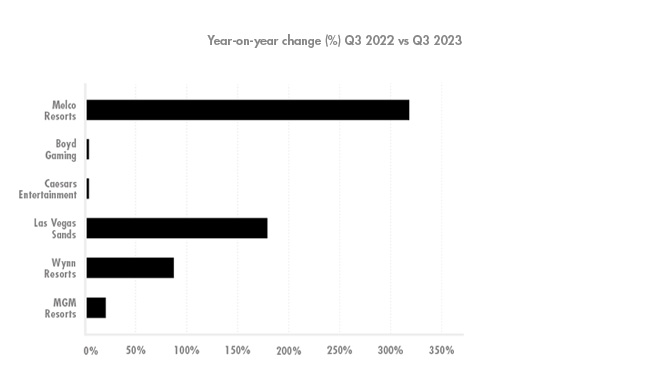

Year-on-year change (%) Q3 2022 vs Q3 2023

Source: Company reports

- US-majority operators (Boyd Gaming, Caesars Entertainment) have shown the least growth in Q3 2023 in the sample, while operators working mostly in Asia (Las Vegas Sands, Melco) have seen the most significant growth.

- Operators functioning in both territories (MGM Resorts, Wynn Resorts) have taken a middle ground in terms of growth.

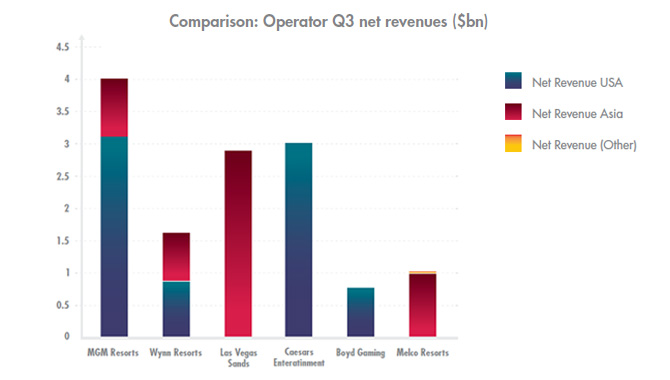

Comparison: Operator Q3 net revenues ($bn)

Source: Company reports

- As the two major operators in Las Vegas, MGM Resorts and Caesars Entertainment have been able to pull in the highest net revenues of Q3 2023 compared to the six in this sample. MGM Resorts also has a notable presence in Asia, through its subsidiary MGM China.

- Las Vegas Sands, which operates exclusively in Asia, is less than $20m behind Caesars Entertainment. Such a high net revenue shows a flourishing market in Asia, beginning to overcome the challenges presented to it in previous years.

- The other net revenue at Melco Resorts accounts for the operators ventures in Europe, specifically Cyprus Casinos.

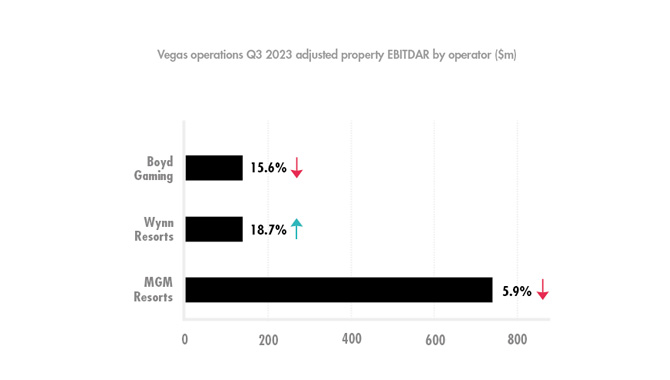

Vegas operations adjusted property EBITDAR by operator ($m)

Source: Company reports

- Adjusted property EBITDAR by operator for Vegas operations has shown growth overall, with Wynn Resorts making the most notable growth.

- Compared to this time last year, only Wynn Resorts saw an increase in adjusted property EBITDA. Both MGM Resorts and Boyd Gaming saw decreases in this metric, down 5.9% and 15.6% year-on-year respectively.

MGM vs Wynn adjusted property EBITDAR ($m) Q3 2022 vs Q3 2023

Source: Company reports

- With Covid-19 restrictions mostly lifted in China, Macau has been able to re-establish its financial earnings and return to revenue levels similar to those pre-Covid.

- While MGM Resorts was able to report earnings in Q3 2023 higher than those reported in Q3 2019, this is not reflective of the industry as a whole post-Covid. It is instead a reflection of the growth specific to the company and its unique circumstances.

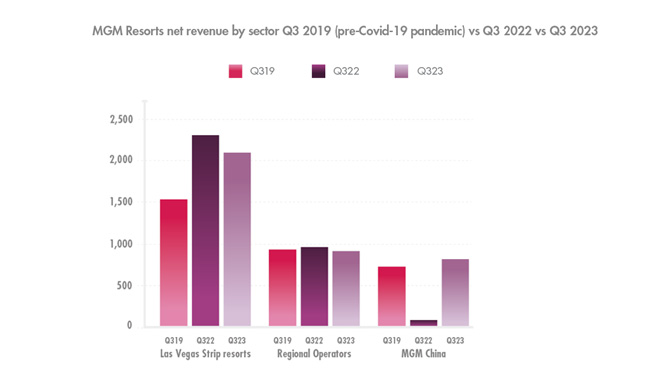

MGM Resorts net revenue ($m) by sector Q3 2019 vs Q3 2022 vs Q3 2023

Source: Company reports

- It is no surprise that MGM Resorts’ Las Vegas resorts have pulled in the majority of its income. Properties include the Bellagio and Mandalay Bay, some of the most notable properties on the Las Vegas Strip.

- When it comes to percentage growth, however, MGM China has been the most successful. The sector’s year-on-year net revenue was up 829%, compared to Las Vegas, which had a net revenue decrease of 8.5%.

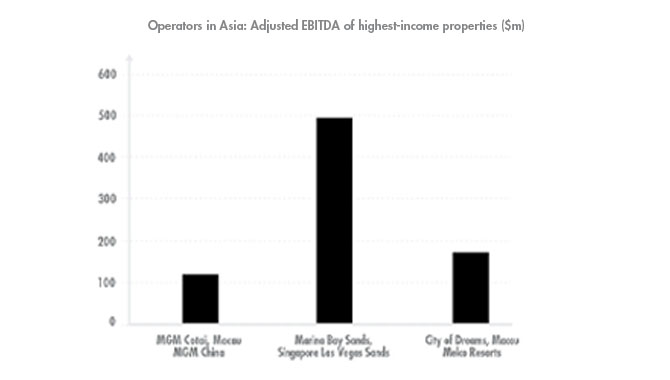

Operators in Asia: Adjusted EBITDA of highest-income properties ($m)

Source: Company reports

- Despite all the successes seen in Macau, it is Marina Bay Sands in Singapore that has the most notable adjusted EBITDA of a single property in Asia of the six operators under analysis.

- Even if the adjusted EBITDA of MGM Cotai and City of Dreams were combined, they would not equal that of Marina Bay Sands.

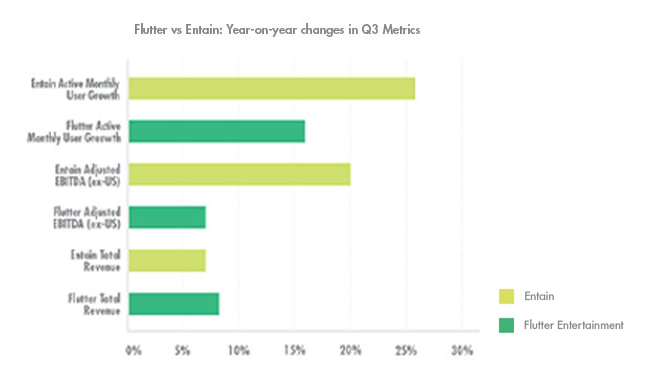

Flutter vs Entain: Year-on-year changes in Q3 Metrics

Source: Company reports

- Flutter Entertainment’s primary non-US territories include the UK, Ireland and Australia, whereas for Entain, territories include Brazil, Central and Eastern Europe and New Zealand.

- The year-on-year change at Flutter and Entain shows that regulated markets around the globe outside of the US are growing, particularly Europe and LatAm.

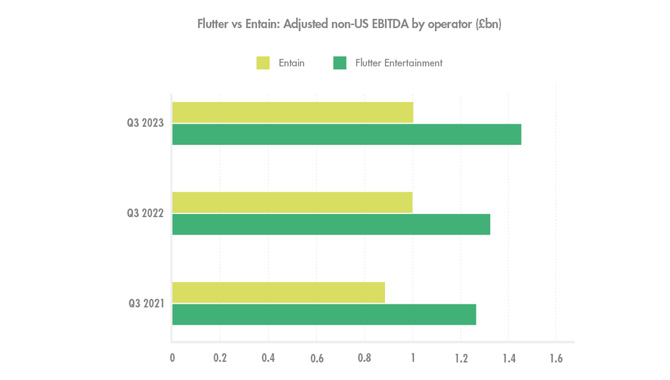

Flutter vs Entain: Adjusted non-US EBITDA by operator (£bn)

Source: Company reports

- Adjusted EBITDA for Entain has been particularly stagnant over the past three years. Meanwhile, Flutter Entertainment has seen slow but steady increases year-on-year.

- Flutter Entertainment put its growth in Adjusted non-US EBITDA down to the strong UK & Ireland market. This is despite revenue from Australia being down in Q3 2023.

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.