Facing Facts: The history of iGaming in numbers

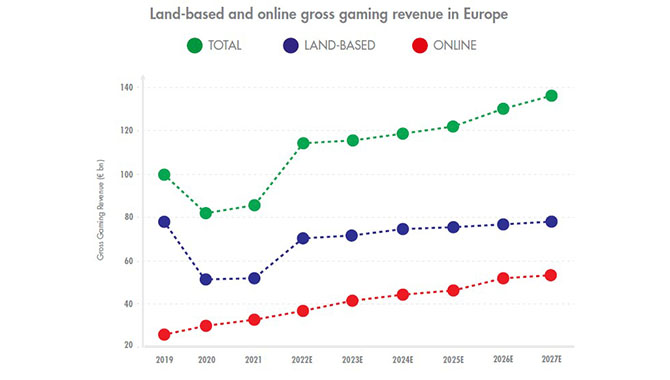

Land-based and online gross gaming revenue in Europe

Source: European Gaming & Betting Association

Online gaming has grown steadily since 2019, being able to avoid the revenue dips faced by land-based casinos in 2020 and 2021 due to the Covid-19 pandemic. Despite this, land-based gaming in Europe is still the dominant market force.

After its bounce-back in the post-Covid market, land-based casino revenue growth in Europe has remained steady, on far less steep an incline compared to online gaming. Were these trajectories to continue beyond 2027 predictions, there may be a point when online gaming outperforms land-based casinos in Europe.

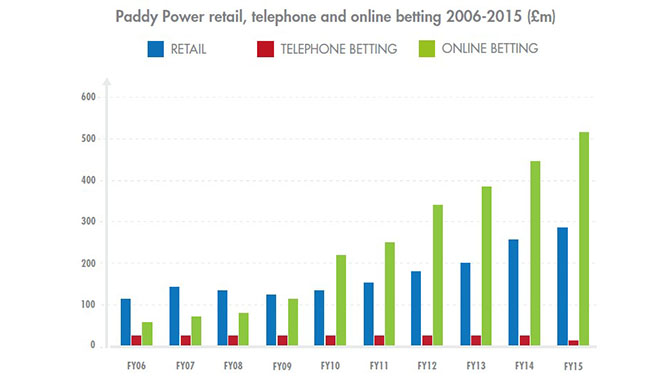

Paddy Power FY gross profit, 2006 – 2015 (€m)

Source: Company reports

Paddy Power began taking online bets in 2000, with online betting overshadowing telephone betting in terms of turnover (handle) by 2003. By 2011, with the advent and proliferation of smartphones around the time, online betting also came to overshadow retail betting.

In 2016 Paddy Power merged with Betfair in February 2016 to become Paddy Power Betfair plc. This would later become Flutter Entertainment.

While retail and online betting grew, telephone betting remained mostly stagnant, facing a slow decline before FY gross profit dropped sharply in 2015. During a key period in the brand’s history, online betting soared…

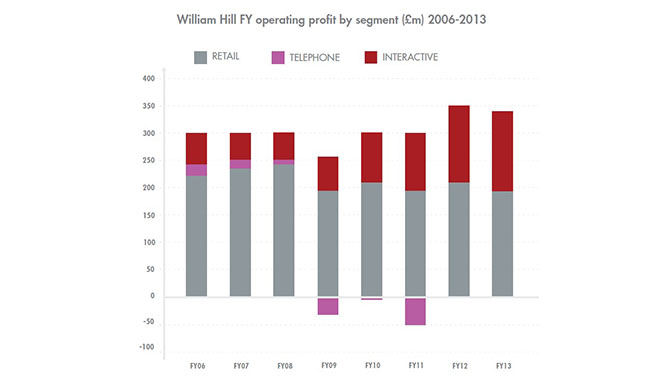

William Hill FY operating profit by segment (£m) 2006 –2013

Source: Company reports

William Hill was founded in the early 1900s offering bookie services in the UK. It introduced online betting options (called ‘interactive’ in early company reports) in the late 1990s, which resulted in the rapid decline and eventual operating loss of telephone betting.

Telephone betting was reported to have made £0.0m in FY12, with no report given in 2013.

While profits fluctuated in the period at around the £300m mark, the contributors to this amount shifted, with retail profit declining while online profit grew annually. This grew notably between 2010 – 2012 with the introduction of smartphones.

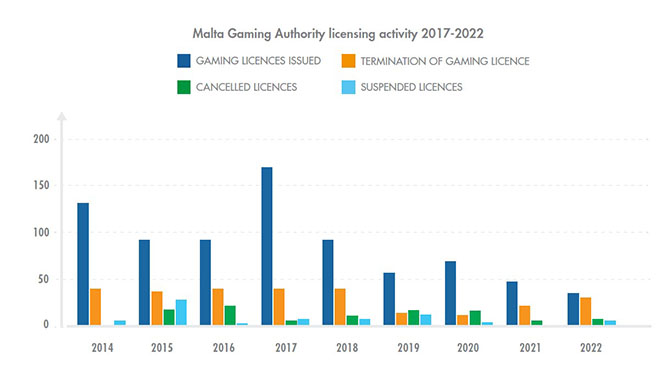

Malta Gaming Authority licencing activity, 2017 – 2022

Source: Malta Gaming Authority

The Malta Gaming Authority was established in 2001. The nation became an iGaming hub at the time with iGaming now being a key industry on the island. A gaming licence from the MGA allows operators and suppliers to work in several European territories.

Fewer licences were issued in 2022 than any other year listed at 31. Despite this, 2022 saw 27 gaming licence terminations.

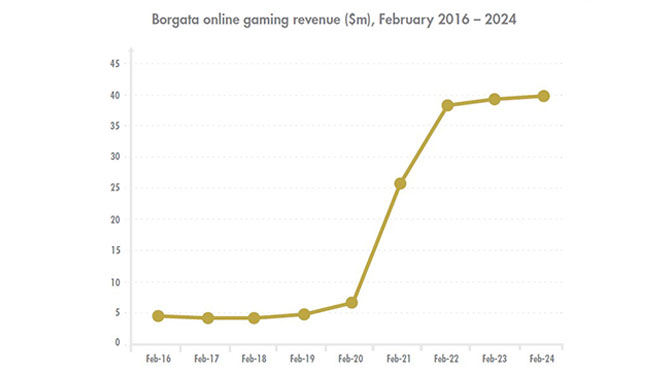

New Jersey online gaming revenue ($m), February 2016 – 2024

Source: New Jersey Division of Gaming Enforcement

Despite New Jersey Governor Phil Murphy signing Assembly Bill 4111 to legalise sports betting in the Garden State, Borgata Hotel Casino & Spa, the most profitable casino in the state, did not see an uptick in online gross monthly win until 2020. This may, in part, be due to the impact of Covid-19 and the demand for online gaming services.

Following growth between 2020 and 2022, monthly gross internet win seems to have stabilised in New Jersey, with Borgata reporting revenue at around the $40m mark in both February 2023 and 2024. These figures show the glowing potential of iGaming within the US… which is only yet touching the surface.

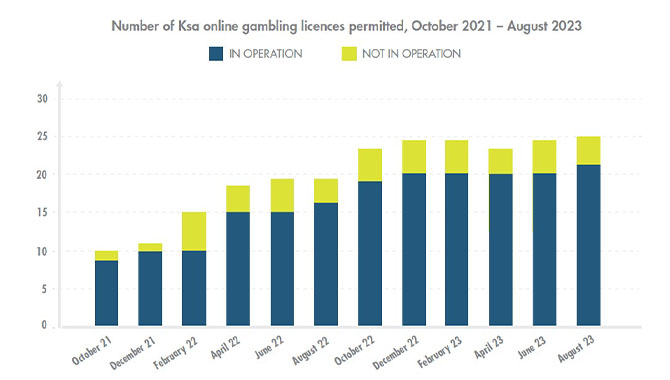

Number of Ksa online gambling licences permitted, October 2021 – August 2023

Source: The Kansspelautoriteit

Online gambling became legalised in the Netherlands in October 2021, with the Kansspelautoriteit (Ksa) providing 10 licences at launch. Some of the first operators to receive a Dutch licence included bet365 and the Dutch lottery, Nederlandse Loterij. ‘In operation’ refers to operators who began operations upon receiving a licence, while ‘not in operation’ refers to operators who had not started operations at the time of receiving its licence.

While growth was notable in the first year of legal online gaming, more than doubling from October 2021 to October 2022, the number of licences has since levelled out, with only one new licence permitted between December 2022 and August 2023.

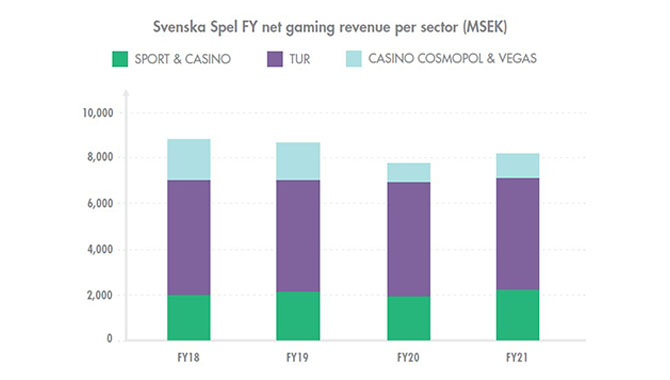

Svenska Spel FY net gaming revenue per sector (MSEK)

Source: Company reports

Svenska Spel is a Swedish government-owned gaming operator that has been in operation since 1997. Sport & Casino and Tur (lottery and number games) results include both land-based and online revenue.

Vegas is Sweden’s only legal slot game and operates in pubs, bingo halls and restaurants in Sweden, while Casino Cosmopol is a chain of legal land-based casinos operating across Sweden.

Land-based operations (Casino Cosmopol & Vegas) were the most significantly impacted by Covid-19, as seen by the fall in revenue from SEK1.72bn in FY19 to SEK0.89bn in FY20.

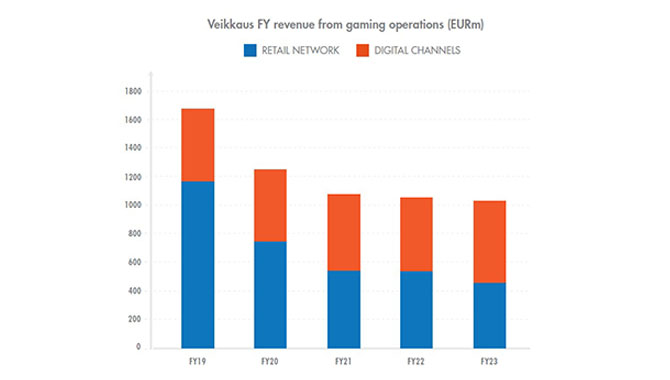

Veikkaus FY revenue from gaming operations (EURm)

Source: Company reports

Much like neighbouring Sweden, Veikkaus, Finland’s government-owned monopoly gaming operator, saw a fall in land-based gaming revenue during Covid-19 while operations with more online capabilities remained stable.

While gaming revenue has fallen overall, down from €1.69bn for FY19 to €1.03bn for FY23, the split between revenue from online and retail operations has shifted notably. While in 2019 retail accounted for 68% of annual revenue, in 2023 it only accounted for 45.2%.

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.