Facing Facts: Online gaming trends in the last decade

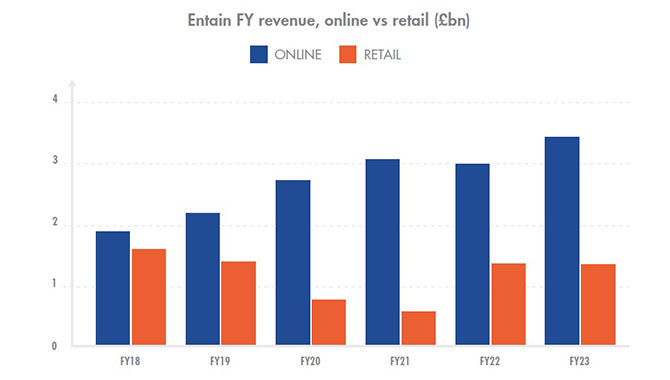

Entain FY revenue, online vs retail (£bn)

Source: Company reports

By looking at Entain’s FY results since 2018, we set a basis for the significance that online gaming plays in the overall market. Prior to the Covid-19 pandemic, online and retail gaming existed on fairly level playing fields. Now post-Covid, while this market has recovered it has still not reached pre-Covid levels, while online gaming has grown 75.5%.

2018 also marks the founding of BetMGM, Entain’s online gaming venture with MGM Resorts. In FY23 BetMGM’s net revenue was up 36% year-on-year for a total of $1.96bn – more than the entirety of Entain Group’s FY23 retail revenue.

2018 also saw the legalisation of sports betting in the US, significantly contributing to the growth of online gaming revenue due to the range of mobile sportsbooks available.

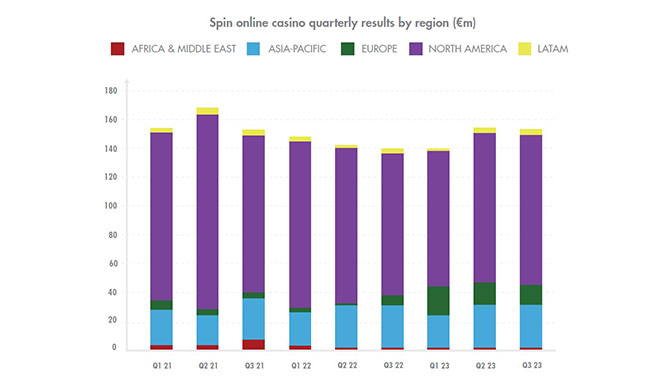

Spin online casino Q1, Q2, Q3 comparisons by region (€m)

Source: Company reports

Spin, an online casino and subsidiary of Super Group, offers games around the world, with its largest market for online casino being North America. However, more often than not the Asia-Pacific area is shown to generate more online casino revenue for Spin quarterly than Europe.

Due to the size of the Muslim population it is understandable why the Africa & Middle East area generates very little quarterly compared to other regions.

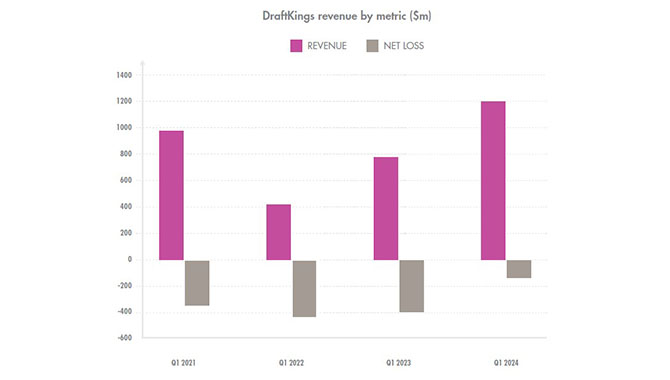

DraftKings revenue by metric ($m)

Source: Company reports

Declines in net loss and increases in revenue are a trend for DraftKings across the last four quarters, with Q1 2024 revenue almost 3.8x higher than what was reported in Q1 2021.

2022 provides a notable outlier, with net loss increasing from the year prior while experiencing growth less significant than that seen across other quarters. This may explain business decisions made after the quarter, such as acquiring Golden Nugget Online Gaming and launching iGaming in Ontario.

Between Q1 2023 and Q1 2024, DraftKings’ revenue grew by 52.7%. But, when will DraftKings turn a profit?

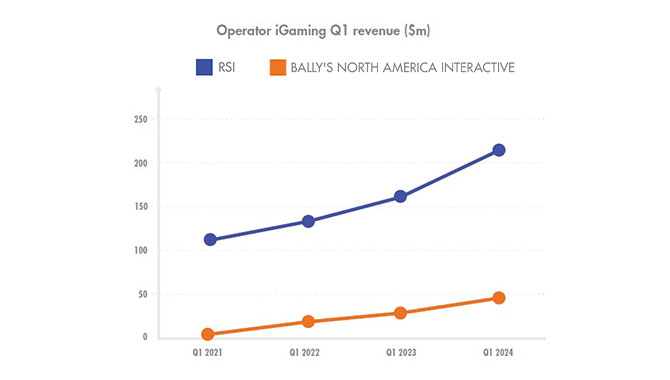

Operator iGaming Q1 revenue ($m)

Source: Company reports

By taking the data accumulated from the five iGaming states over a decade as seen above, Analysis Group has made projections of what iGaming revenue could look like in five different states, were it to be legalised. While Bally’s North America Interactive and RSI both show similar patterns of growth, between Q1 2023 and Q1 2024 RSI experienced a notable spike in revenue, totaling $217.4m with a year-on-year growth rate of 33.9%. Several explanations for this growth include increased partnership activity in 2023, with examples including Play’n Go, Hacksaw Gaming and the Delaware Lottery.

Bally’s North America Interactive is separate from Bally’s International Interactive, which routinely reports quarterly revenue of $200m+.

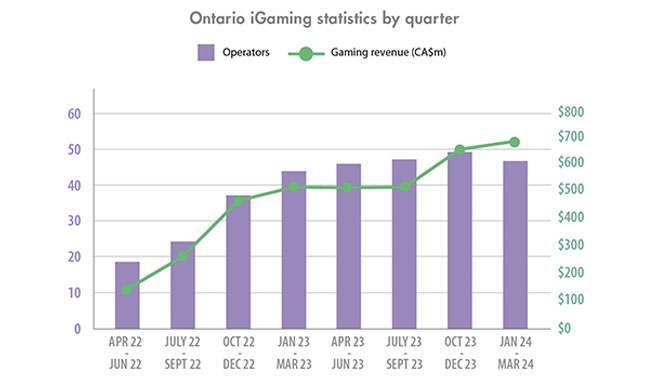

Ontario iGaming operators and gaming websites by quarter

Source: iGaming Ontario

The Canadian province of Ontario was the first to legalise and regulate in Canada in April 2022. In the first quarter (until 30 June, 2022) the province generated CA$162m (US$118.9m) in gaming revenue, with 18 operators and 31 gaming websites.

Growth was rapid across the first year, with a sharp incline in websites. However, this growth slowed down and even declined in some quarters the following year as operators faced the realities of navigating this emerging market.

Ontario has been a popular destination for overseas iGaming operators to launch in North America before taking on the States. Since its first Q1 report, operators and gaming websites have more than doubled.

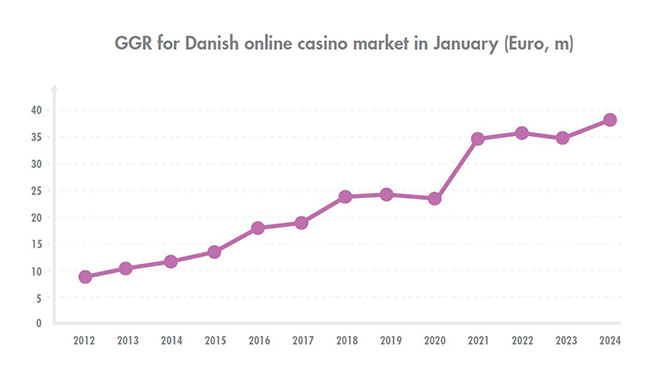

GGR for Danish online casino market in January (Euro, m)

Source: Danish Gambling Authority

Growth of iGaming revenue in Denmark remained steady between 2012 and 2016, settling in 2017 before growing again until 2020. As seen across many of these reports, Covid-19 saw the dramatic increase of iGaming revenues across the world, before settling somewhat post-pandemic.

In 2021 online gaming taxes in Denmark grew from 20% to 28%, being a potential factor in the slowdown of GGR growth in the coming years.

Denmark opened its iGaming market in 2011 following approvals of new regulations by the EU, dissolving the monopoly system that was previously in place. Today, Finland and Norway are also working towards dismantling their gaming monopolies in favour of a licenceing system.

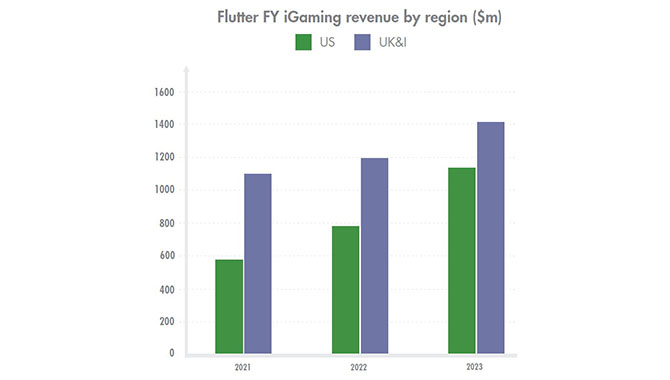

Flutter FY iGaming revenue by region ($m)

Source: Company reports

With iGaming only legalised in seven states, it should not be overly surprising that the UK and Ireland generate more in iGaming revenue for Flutter than the US.

The US market for Flutter is also very heavily influenced by FanDuel, the biggest mobile sportsbook in the US by market share. When looking at Flutter’s annual revenue overall, the US notably outperforms any other region. In 2023 for example, US operations accounted for over a third of the company’s total revenue.

Growth in US iGaming revenue is more sizeable annually than growth in the UK and Ireland, in part due to the steady growth of iGaming legalisation across the states. Michigan legalised iGaming in 2021, while Rhode Island legalised iGaming in 2024. Could that see Flutter’s US iGaming revenue catch up with the UK and Ireland by the end of the year?

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.