Facing facts: FY revenue figures reflect a turbulent ’24

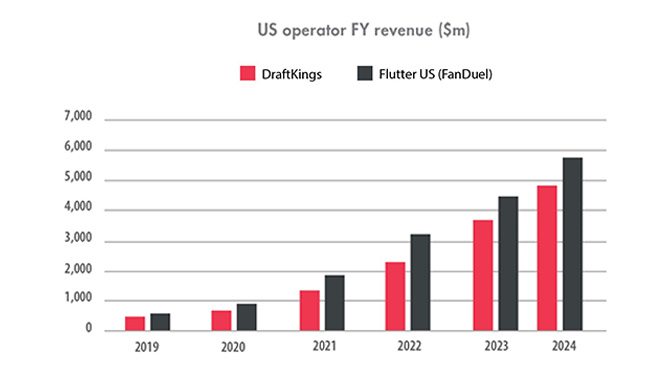

US operator FY revenue ($m)

Source: DraftKings, FanDuel

*All FanDuel numbers from 2021 and prior converted from GBP at rate accurate as of 06.03.2025. All revenues represent US only

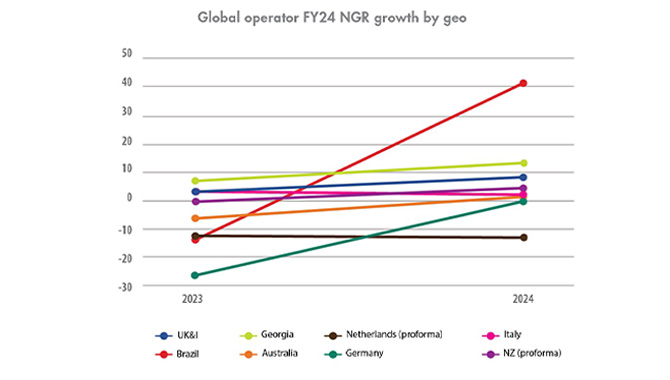

Global operator FY24 NGR growth by geo

Source: Entain

While most of Entain’s territories of operation have seen slight increases in online NGR year-on-year, one in particular stands out. This, unsurprisingly, is Brazil. In 2023, NGR was down 14%, while in 2024, it was up 41%. Of course, with last year seeing the development of a regulated framework for online gaming in the nation, which was put into action on 1 January 2025, this makes sense — and, given effects across the market by operators to make the most of this new regulated territory, it is likely that this growth will continue.

Only the Netherlands on a proforma basis saw an increase to its NGR decline, from –12% in 2023 to –13% in 2024. While a minimal difference, continued decline suggests a territory that is presenting continuous challenges, and a challenge that Entain has yet to overcome.

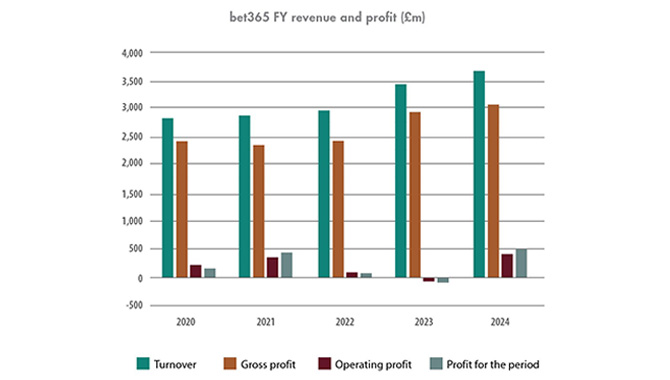

Operator bet365 FY revenue and profit (£m)

Source: bet365

Between the 2020 – 2022 financial period, bet365’s turnover changed very little, from £2.81bn ($3.6bn) in 2020 to £2.87bn in 2022. However, FY23 saw turnover jump significantly, up 18.8% to £3.41bn. Turnover jumped 9% the following year, coming to £3.72bn.

In 2023, bet365 reported both an operating loss and loss for the financial period, at £37.3m and £69.4m respectively. This was put down to the costs of entering new markets, IT development and increased staff costs. However, with operating profit and profit for the period surpassing 2021’s results in 2024, it seems the increased costs yielded the desired results.

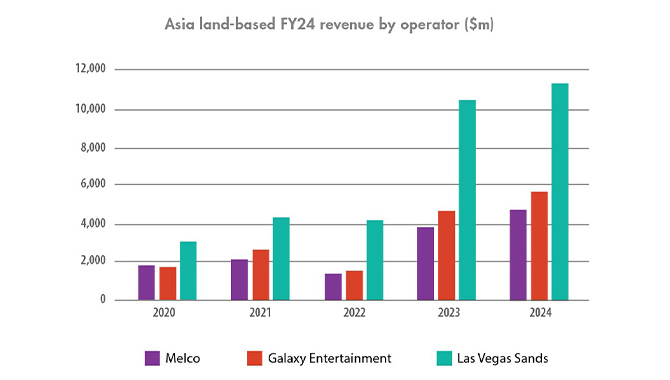

Asia land-based FY24 revenue by operator ($m)

Source: Company sites

*All Galaxy Entertainment numbers converted from HKD at rate accurate as of 10.03.2025

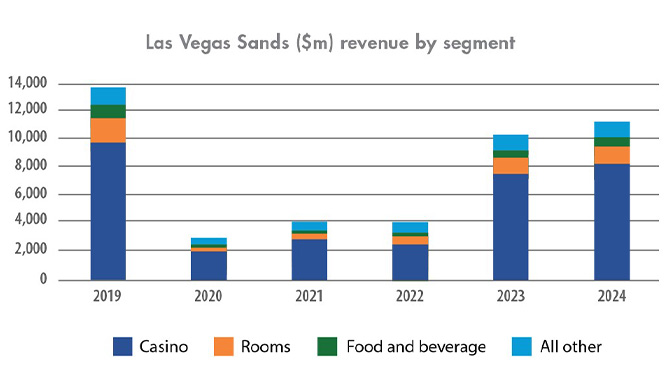

Unsurprisingly, Las Vegas Sands outperformed its competitors by a significant margin, though it is important to note that on top of its Macau properties, including The Venetian Macao and Londoner Macao, it is also the operator of Marina Bay Sands, a property that made $4.23bn in FY24 alone – roughly $400m less than the entirety of Melco’s 2024 operations.

Despite the difference, growth across the three operators’ revenue year-on-year remains relatively similar. For example, FY24 revenue was up 8.9% for Sands, 21.7% for Galaxy Entertainment and 22.9% for Melco. The two smaller operators grew at a similar pace, while Sands followed slightly behind; a common trend among the largest operators.

Asia FY revenue by segment ($m)

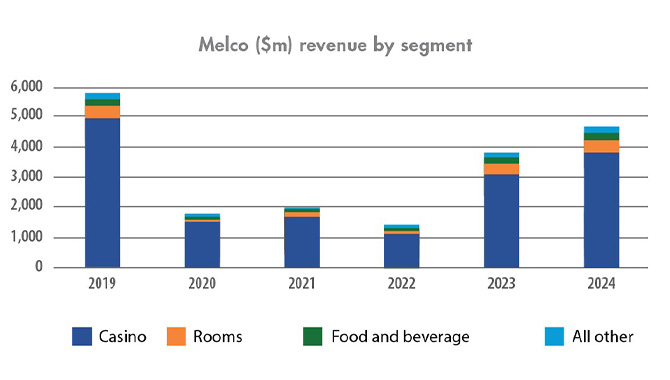

Melco ($m) revenue by segment

Source: Melco

Comparing Melco to Las Vegas Sands, unsurprisingly, both generated the largest portion of their revenue from casino games. However, especially before Covid-19, it was clear this was even more so the case for Melco, with casino revenue accounting for 86.8% of the total.

Las Vegas Sands ($m) revenue by segment

Source: Las Vegas Sands

The Macau Government has created post-Covid initiatives to diversify revenue streams in the area, with many hotel casinos placing emphasis on non-gaming options. However, this growth has been somewhat limited. Melco’s other revenue sources, including retail and entertainment, were only up $6m between 2023 and 2024, though food and beverage saw a notable increase in earnings, up 36.8% to $286m. This is reflected in several accolades received by the operator, with Melco receiving eight stars in Michelin’s 2024 Hong Kong & Macau guide.

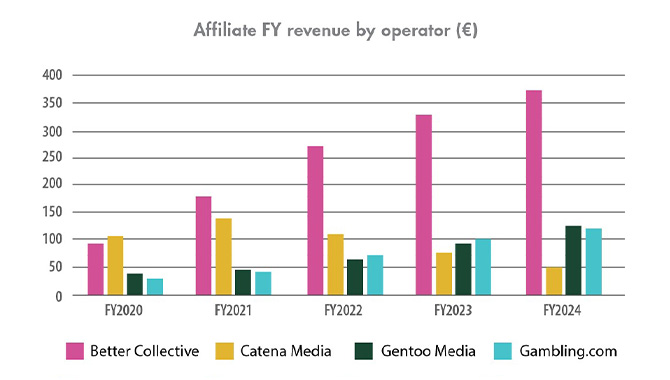

Affiliate FY revenue by operator (€)

*All Gambling.com numbers converted from USD at rate accurate as of 10.03.2025

The affiliate market has experienced a mixed bag over the past few years. Post-Covid, Better Collective has carved a path to being one of the sector’s biggest affiliates in terms of revenue, making €371.5m ($402.7m) in FY24 – more than Catena, Gentoo and Gambling.com combined.

Catena Media has faced challenges since 2022, in part due to declines in its US segment, which accounts for the majority of its revenue. Indeed, even Better Collective has noted challenging US conditions. Yet, despite reporting its results in dollars as opposed to Euro’s, Gambling.com, which was reporting a quarter of the revenue made by Catena in 2020, has surpassed Catena Media two years running.

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.