Beyond the odds: What are the pros and cons of selling bet365?

Industry giant has been valued at £9bn and linked with a partial or full sale, motivated by US expansion. But what would bet365 gain – and what could be lost?

Key points:

– Sale and potential US listing could signal final stage of major US push, as operator engages in full-scale competition with market leaders FanDuel and DraftKings

– Could difficult US landscape be a factor as well as US promise?

– Blackstone, Apollo, DraftKings, Caesars or MGM could top list of realistic gaming-related buyers

– Sale should not undermine core tenets of bet365 success to date: agility, skilled trading and a high-quality product

When deciding how big a news story is, the Gambling Insider editorial team has a running joke that if DraftKings buys FanDuel, we drop everything.

It serves as a good example because, in practice, such a deal is almost impossible. Just a few months ago, however, one might have said the same about the sale of bet365.

Long since a market leader in the UK, generating strong revenue across global markets and strategically placed in various states across the US, bet365 has represented the pinnacle of online, and certainly in-play, betting for years.

Yet reports last week suggested CEO Denise Coates and the Coates family are considering either a partial or full sale of the operator – with the business valued at £9bn ($12bn).

That figure is no small sum but, for a brand that generated £3.72bn in turnover for its 2024 financial year, you could be forgiven for expecting a higher number.

The road to selling?

The notion that bet365 is ready to sell has surprised analysts across the City of London, according to the Sunday Times, but it is not a total shock given this year’s developments.

Indeed, the industry giant recently announced it will be leaving Asian markets such as China, while it has been turning more and more of its focus towards the US.

This, in itself, does not guarantee an M&A strategy. Were Denise Coates to remain in charge of a privately run bet365, that organisation would have as good a chance as any global brand of challenging current US leaders FanDuel and DraftKings.

But the US product itself is a little different. The operator may require adaptation, as well as assistance from a US partner that knows its markets better and is able to engage effectively with US regulators.

This is where US involvement makes sense. Although the Sunday Times reports that JP Morgan and Jefferies were “completely unaware” that Coates had launched a “beauty parade” for investors, a partial sale ahead of an eventual US listing has been mooted as a long-term strategy.

The financial benefits

It was the Guardian that originally broke the story of bet365 looking to sell. The news is still being treated with scepticism among City traders, while the Daily Telegraph has argued that the Labour Government must do everything it can to persuade Coates to remain in the UK.

According to these reports, a deal could eventually land Coates £5bn+.

As we can also see from the above data, 2024 revenues from across the industry paint a favourable picture for a potential merger.

Later in this article, we will explore the potential drawbacks of a sale – but the numbers do paint a clear picture. For all of bet365’s success, Flutter is perhaps the example it will look to follow. Flutter’s US division (FanDuel) outearned bet365 in the US alone, while DraftKings generated slightly less than bet365’s global total, again, solely in the US.

Global operators that no longer hold B2C operations in the US, FDJ United (owner of Kindred Group) and Betsson, serve as a lowlier comparison, while BetMGM generated $2.1bn for 2024 in the US.

One of BetMGM’s two owners, Entain, reported $6.66bn in 2024 revenue, again some way off Flutter but outpacing bet365, helped by BetMGM’s US revenue.

While bet365’s figures represent its 2024 Financial Year – a slightly different time period – it is the closest comparison we have and it still makes a clear point.

What is most impressive is that bet365’s figures represent just one brand; but in moving to the next level financially, it has been suggested that it may have to start thinking more like a ‘group.’

Would the timing be right?

The reasoning behind a potential sale may also lie in the difficulties of the US market, as well as its promise.

There is a perception outside the industry that the US is flying high on its way to becoming the most lucrative online gambling region in the world. But the reality right now is a little different.

The US splits up into 40+ different markets, all with varying regulations and requiring a specific focus. The state with the highest mobile betting across the US, New York, regularly posts around $2bn in monthly handle – but taxes mobile sports betting revenue at a hefty 51%.

Meanwhile, online casino is only legal in seven states and the sports betting landscape is dominated by FanDuel and DraftKings, with Entain/MGM joint venture BetMGM, Caesars, Fanatics, ESPN Bet, and occasionally brands like Rush Street Interactive and Bally’s scrapping for the remains.

To emphasise what the US is missing, BetMGM generated $1.47bn in iGaming revenue for 2024 in just a handful of states, compared to $554m in sports betting revenue across multiple states throughout the country.

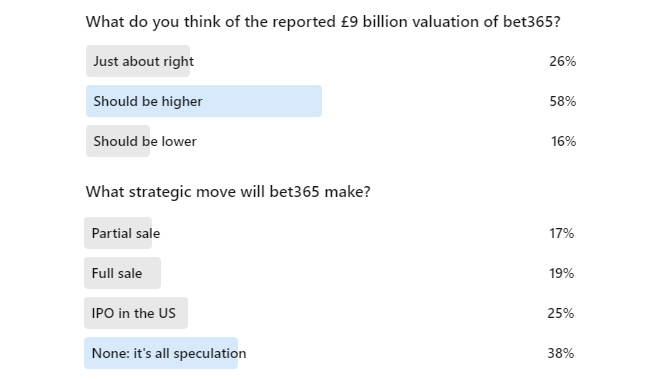

LinkedIn votes show Gambling Insider readers are not necessarily convinced by the valuation nor the idea of a takeover itself

The appeal of the market as it stands presents more barriers to growth than Latin America and, specifically, Brazil.

And let us not forget the biggest headlines in US gaming right now: predictions market operators like Kalshi bidding to get sports event contracts regulated under the Commodities Futures Trading Commission. This would provide said firms with the ability to essentially circumvent sports betting regulations nationwide – completely bypassing sports betting brands who have spent years building up local presences following state-by-state laws.

Headlines are similarly being created by sweepstakes casino operators (and daily fantasy sports brands like PrizePicks) that have generated billions across the US, in a manner that both tribal and commercial gambling organisations feel is unlawful.

Who could buy bet365?

When Flutter bought a 58% stake in FanDuel for just $158m in May 2018, the timing was perfect. PASPA was getting overturned, competition was minimal and FanDuel already had a huge fantasy player database to lean in to.

The landscape is a little different for bet365 today. This is why the motivations of the Coates family become a crucial driver behind any deal. At 57 years of age, if Denise Coates wants to crown a hugely successful career by selling up and reducing her day-to-day duties, this is her chance.

Exactly how involved Denise Coates wants to be in day-to-day activities is a factor that adds to any financial picture

If the idea, however, is for bet365 to keep competing on a global scale with the Coates family at the forefront, its agile nature as an innovative private company, possessing its own proprietary technology, could be enough for bet365 to go it alone.

Besides, who could actually have the firepower to buy bet365? For starters, the likes of Flutter and Entain would likely be stopped by anti-monopoly watchdogs in the UK.

As the Sunday Times notes, DraftKings could be a theoretical buyer. It does have history here, as it tried to purchase Entain in 2021. But, while bet365’s online prowess could help DraftKings leapfrog FanDuel into the #1 position, Jason Robins’ organisation regularly reports quarterly losses, meaning it is not necessarily sitting on the resources needed to fuel the acquisition.

Funds like Blackstone Capital Partners or Apollo Global Management could be realistic options. Neither firm, though, has yet to add a true B2C global leader to their respective portfolios, and Apollo has missed out on several high-profile brands (notably Caesars) in the past.

The mention of Caesars is interesting, as one of the biggest names in global land-based gambling combining with an online giant like bet365 could make huge sense. Caesars’ online product is not troubling the likes of FanDuel or DraftKings, with BetMGM further ahead in that race than Caesars Digital.

The BetMGM joint venture with Entain would also complicate matters were MGM Resorts to take an interest. But, by all other accounts, an MGM-bet365 match up would shake up the industry. Perhaps even enough to sell full ownership of BetMGM to Entain and combine bet365’s technology with that of LeoVegas, or going for broke and taking full ownership of BetMGM as well as bet365.

How would the UK market be impacted?

One factor worth considering is bet365’s dominance in the UK. Bill Barber, Industry Editor at the Racing Post, has warned that any new bet365 owner may take a reduced interest in UK horseracing industry – a sector bet365 is a huge supporter of.

But bet365 itself has need for caution. What has driven its success thus far is technological agility, speed and innovation across its departments. Conversations Gambling Insider has held within the industry emphasise bet365’s high levels of staff retention and the fact that its trading ability ranks so well compared to competitors.

The company is private by name and nature, with CEO Coates even refusing to give any public interviews. That would immediately be lost were a high-profile US investor or acquirer to take over.

Brands like Ladbrokes, Coral, Sky Bet, William Hill and Paddy Power would suddenly have genuine hope of trying to lead the market if bet365 saw any sort of slowdown during or after its takeover.

Should bet365’s owners sell?

If the Coates family feels its independent gambling journey is complete, and that a US-based future requires extra investment or external expertise, a new betting beast may be born that can truly challenge FanDuel and DraftKings.

Equally, there may be plenty to lose, explaining the surprise and scepticism of traders across the City of London.

In today’s market, there is much to gain from staying private, especially considering the Latin American opportunity taking the industry by storm.

But the numbers do not lie. If bet365 believes extra investment and a US listing will help it go toe to toe across the Atlantic Ocean, the opportunity is certainly there.

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.