Genius Sports Pushes Back on Investor Criticism of $1.2B Legend Deal in Q4 Earnings Call

Genius Sports used its Q4 earnings call to defend its $1.2B Legend acquisition after investor skepticism.

After posting its strongest revenue growth since 2021 and its highest-ever adjusted EBITDA margin as a public company, Genius Sports used its Q4 earnings call to address its planned acquisition of Legend, valued at up to $1.2 billion, arguing the platform offers valuable user engagement, data advantages, and significant growth opportunities.

Investors reacted skeptically when the company announced the agreement on Feb. 5, wiping $600-700 million off Genius’ market cap in the immediate aftermath.

During the March 4 Q4 earnings call, executives pushed back on critics who compared the deal to buying a traditional affiliate business. Genius expects the deal to close in Q2 2026, pending regulatory approval.

Management estimates that annualized group revenue will reach about $1.1 billion after closing, with adjusted EBITDA of $320- $330 million, resulting in a margin of roughly 30%.

Genius Sports reported full-year 2025 revenue of $669 million, marking a 31% year-on-year increase. The company also expanded its adjusted EBITDA margin to 20%. Much of the discussion on the call focused on management’s effort to frame the Legend acquisition as a technology deal rather than a media acquisition.

Defending the Legend Deal

CEO Mark Locke had already issued a letter to shareholders on Feb. 18 explaining the logic behind the Legend acquisition. He pointed to similar investor skepticism around previous deals that later proved successful.

Locke continued that message during Wednesday’s earnings call, saying the company wanted to “address[] directly the key questions raised by investors”. He contrasted traditional affiliate sites, which rely heavily on SEO and paid marketing, with Legend’s model.

Traditional affiliates often spend 30-40% of their revenue maintaining traffic, while Legend spends “approximately 5% because its traffic is direct and repeat.” Locke said the platform attracts 118 million users who arrive directly and return regularly.

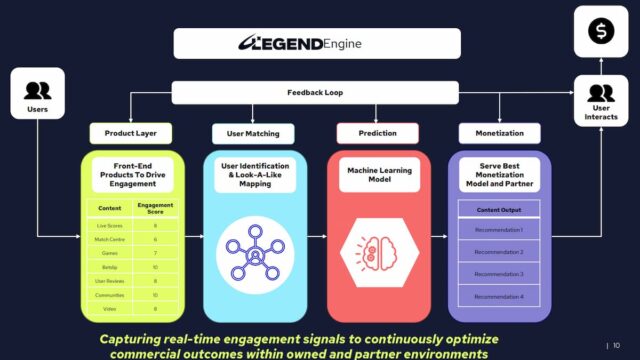

Locke argued that “Legend is not simply just a media business. It’s a technology company that’s built around large, loyal sports and iGaming audiences,” centered on participation rather than static content. “This content is not static information pages,” he said. “They are environments that are built for participation around live sports and gaming experiences.”

Legend has invested more than $300 million and spent over a decade building an engagement platform where users participate in live esports and iGaming experiences rather than simply viewing pages. Locke described the company’s core advantage as a data-and-optimization feedback loop.

“That feedback loop is where long-term value is created. It’s not about answering factual queries; it’s about facilitating participation inside owned environments and continuously improving the economics behind it.”

Locke cited one example involving a major global operator, which he did not name. That operator reported that customers acquired through Legend show a 60% higher value after 1 year than those acquired through other channels.

He also pointed to a gaming brand that integrated Legend into its digital properties, resulting in a 50% increase in revenue within 6 months.

AI Isn’t a Concern

Some analysts raised concerns that AI and changing search behavior could reduce Legend’s traffic. Locke rejected that view. He argued that large language models strengthen platforms where users actively participate and generate behavioral data.

According to Locke, Legend’s 118 million engaged users and its real-time interaction signals make the platform more valuable in an AI-driven environment. As he put it: “Generic answers are free, proprietary behavioral data is not.”

Locke also argued that Legend is less exposed to algorithm shocks than traditional affiliates because “engagement is recurring,” revenue is diversified, and “the economics are built on participation, not page views.”

Growth Opportunities From the Legend Acquisition

Management identified four key areas where Genius and Legend could create new growth opportunities.

First, the deal gives Genius its first direct entry into the online casino market, expanding its total addressable market by roughly 70%. Operators value players who engage with both online casinos and sports betting at roughly 15 times more than sports-only bettors.

Second, management believes that combining Legend’s first-party audience data with Genius’s Fan Graph will create a powerful privacy-compliant audience asset for advertisers. This capability could strengthen existing agency partnerships with WPP, PMG, and Publicis.

Third, Genius plans to deploy Legend’s engagement and conversion platform across its portfolio of more than 400 sports teams and leagues. Management wants to shift the company’s value proposition from simple data distribution to audience activation.

Finally, Genius plans to distribute its own products through Legend’s channels.

A Big In-Play Opportunity

Executives also highlighted near-term opportunities around Genius’s in-play betting product, BetVision. Locke explained that it’s looking to “maximize the commercial returns that we’re getting on it in terms of the sort of 3x the amount of money we get paid on in-play.”

BetVision currently covers about 25,000 events, but the company sees a pathway to 300,000 events as it expands coverage, particularly through esports competitions.

In-play betting represents about 30% of the U.S. market today, compared with 70-80% in Europe. Locke believes that Legend could help accelerate U.S. adoption toward European levels, thereby increasing revenue-share opportunities.

An Anomaly for the Media Segment

Genius Sports’ media segment grew 37% in 2025 to $144 million. Growth accelerated particularly in the second half of the year, with performance nearly doubling compared with H2 2024.

However, management cautioned that it does not expect that growth rate to continue. Executives attributed part of the surge to a mix of new product launches and favorable market conditions.

The company also announced a change in revenue recognition for certain media agreements, shifting from gross reporting to net reporting. While that change will reduce reported topline growth, it should improve margins.

New Partnerships

Genius also announced a new U.S. partnership with Magnite, the largest independent supply-side platform. The partnership will embed Genius’s real-time sports signals directly into Magnite’s programmatic infrastructure.

The company also revealed a partnership with NBC Sports Regional Networks to power AI-driven augmented advertising across 600 live NBA games.

Chief Revenue Officer Josh Linforth described the strategy as building a portfolio of curated deals “where there is just money flow going from all of these campaigns and advertisers across the ecosystem, buying across the Genius audience and inventory.”

Linforth said the portfolio becomes more valuable as more deals activate and additional unique inventory enters the ecosystem.

Executives also pointed to prediction markets as a near-term advertising tailwind. Linforth said the company is “already seeing spend flowing through from advertisers activating in that space,” adding that Genius expects to “capitalize on the spend boom around prediction markets.”

The Genius Sports share price fell 6% on Wednesday after the earnings call.

Performance Snapshot

FY2025

- Revenue: $669 million, a 31% year-on-year rise

- Adjusted EBITDA: $136 million, representing a 20% margin

- Betting revenue growth: 33%

- Media revenue: $144 million, a 37% year-on-year increase

- Americas revenue growth: 41%

- European revenue growth: 20%

2026 Guidance

- Revenue: $810-820 million, around a 22% increase

- Adjusted EBITDA: $180-190 million, about a 36% increase

Pro Forma Combined Guidance (Annualized Post-Legend Deal Close)

- Revenue: Around $1.1 billion

- Adjusted EBITDA: $320-$330 million

Free cash flow conversion (annualized post-close): approximately 50%, according to CFO Bryan Castellani.

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.