Kambi Price Slips on €42.7M Revenue That Misses Estimates, But EBITA and EPS Improve

Kambi Q4 and FY 2025 revenue misses – the gambling tech firm has more cost-cutting to do, as well as work to turn partnerships into profits.

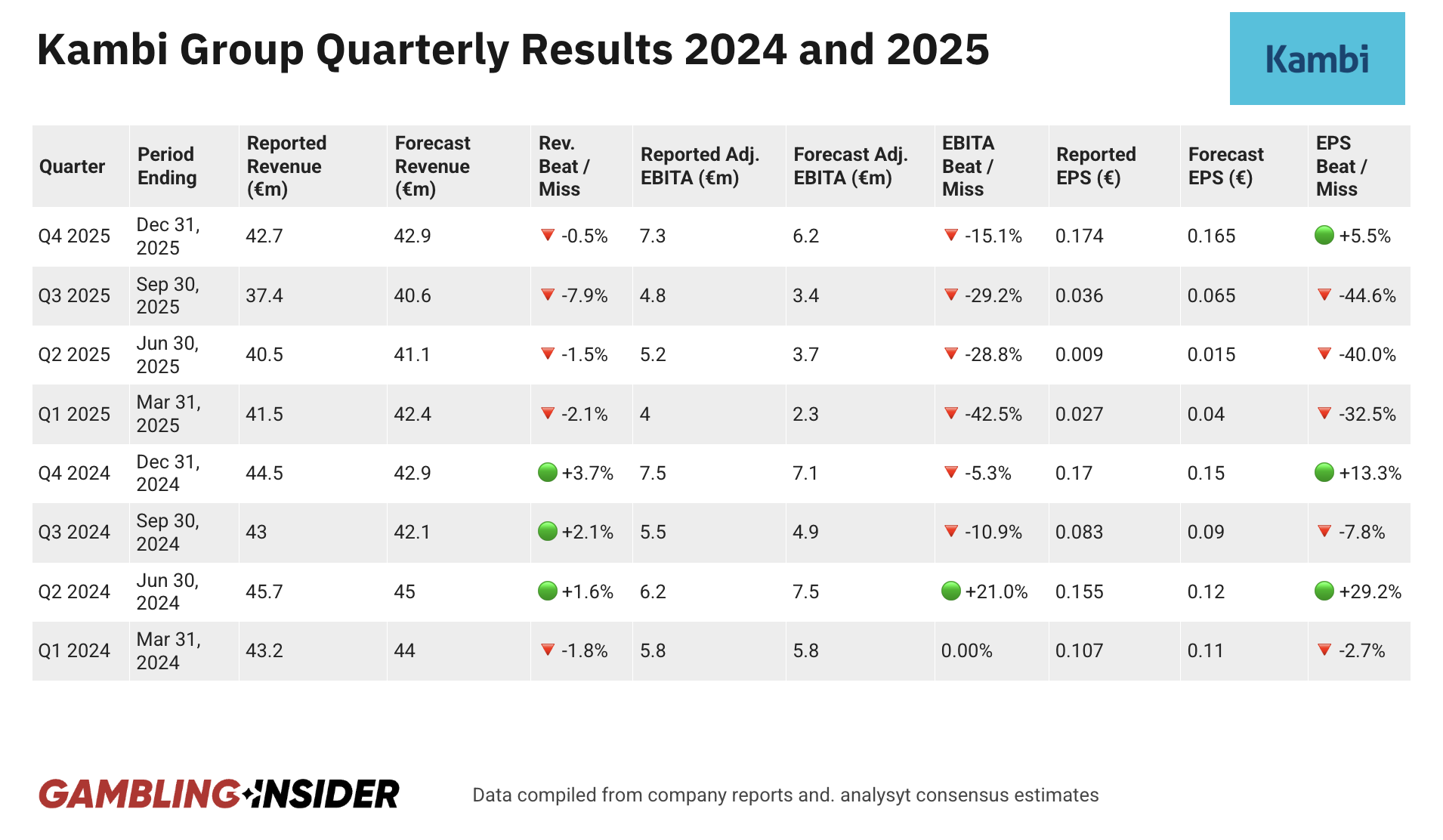

Gambling technology and services company Kambi Group (KAMBI) reported Q4 and full-year 2025 results today, with revenue that missed forecasts by -0.5%, coming in at €42.7 million ($49.86 million) against a forecast of €42.9 million.

The Malta-headquartered company, with major hubs in Stockholm and London, beat on adjusted EBITA, generating just €7.3 million, 17.7% above the €6.2 million forecast. Earnings per share were better at €0.174, up from €0.036 in Kambi’s Q3 results and beating estimates by 5.5%.

Compared to the same period last year (Q4 2024, €6.3 million), adjusted EBITA is €1 million higher. However, on revenue, the story was different. FY 2025 revenue was €162 million compared to €176.4 million in FY 2024.

On a year-over-year basis, full-year adjusted EBITA was also a woeful tale, reporting €17.6 million for the full year, trailing the 2024 figure (€25.4 million) by €7.8 million.

Q4 2025 and full-year cash flow were also down, from €6.7 million to €6.0 million and €25.9 million to €21.2 million, respectively.

Management had previously revised down its 2025 full-year guidance, reducing adjusted EBITA expectations to approximately €17.0 million. The revised estimates were due to FX headwinds and a slower-than-expected rollout of Brazilian regulations.

| Quarter | Period Ending | Reported Revenue (€m) | Forecast Revenue (€m) | Rev. Beat / Miss | Reported Adj. EBITA (€m) | Forecast Adj. EBITA (€m) | EBITA Beat / Miss | Reported EPS (€) | Forecast EPS (€) | EPS Beat / Miss |

| Q4 2025 | Dec 31, 2025 | 42.7 | 42.9 | 🔻 -0.5% | 7.3 | 6.2 | 🟢 +17.7% | 0.174 | 0.165 | 🟢 +5.5% |

| Q3 2025 | Sep 30, 2025 | 37.4 | 40.6 | 🔻 -7.9% | 4.8 | 3.4 | 🟢 +41.2% | 0.036 | 0.065 | 🔻 -44.6% |

| Q2 2025 | Jun 30, 2025 | 40.5 | 41.1 | 🔻 -1.5% | 5.2 | 3.7 | 🟢 +40.5% | 0.009 | 0.015 | 🔻 -40.0% |

| Q1 2025 | Mar 31, 2025 | 41.5 | 42.4 | 🔻 -2.1% | 4 | 2.3 | 🟢 +73.9% | 0.027 | 0.04 | 🔻 -32.5% |

| Q4 2024 | Dec 31, 2024 | 44.5 | 42.9 | 🟢 +3.7% | 7.5 | 7.1 | 🟢 +5.6% | 0.17 | 0.15 | 🟢 +13.3% |

| Q3 2024 | Sep 30, 2024 | 43 | 42.1 | 🟢 +2.1% | 5.5 | 4.9 | 🟢 +12.2% | 0.083 | 0.09 | 🔻 -7.8% |

| Q2 2024 | Jun 30, 2024 | 45.7 | 45 | 🟢 +1.6% | 6.2 | 7.5 | 🔻 -17.3% | 0.155 | 0.12 | 🟢 +29.2% |

| Q1 2024 | Mar 31, 2024 | 43.2 | 44 | 🔻 -1.8% | 5.8 | 5.8 | 0.00% | 0.107 | 0.11 | 🔻 -2.7% |

EBITA Improves on Q3 2025, But Not Enough to Convince Doubters

In the round, the Q4 results are a significant improvement over Q3 (€4.8 million), likely driven by the busy Q4 sporting calendar (NFL, NBA, European soccer) compared to the quieter summer months.

Investors on the earnings call were looking to see if the heavy Q4 sporting calendar helped stabilize the top line. However, YoY comparisons remain difficult due to the loss of major partners (such as PENN Entertainment) and the absence of transition fees that boosted 2024 figures.

In fact, it was mentioned on the call that in December, Kambi, in conjunction with PENN, launched into the newly regulated state of Missouri.

Shareholders are also watching for progress on cost-cutting to protect profitability and margin management amid falling revenues. The jump in adjusted EBITA for Q4 indicates that these efficiency measures are bearing fruit.

Although there were positives on EBITA and new sources of revenue coming into the mix, the revenue miss led to selling. At the time of writing, the stock is trading 1.98% lower at SEK 103.70 ($11.56).

While 2025 can be seen as a transition year for Kambi, Q4 and early 2026 have witnessed a flurry of commercial activity. Investors received updates on how these new deals were being integrated into the business, along with hints about future revenue contributions.

Kambi Partnership Wins for Odds Feed+ Points to Sustained Commercial Momentum

Recent partnership wins include Glitnor Group, a significant turnkey sportsbook win replacing an incumbent provider. Another is ComeOn Group, which was announced this month. It represents a major Odds Feed+ partnership win – Odds Feed+ is Kambi’s premium betting odds feed solution.

And at Ontario Lottery (OLG), Kambi recently replaced FDJ UNITED as the sportsbook partner.

Management was asked to articulate the timeline for when these partners will start contributing to the bottom line and how they will impact Q1 2026 and beyond.

CEO Werner Becher highlighted 15 new partnerships since the start of Q4 2025, an encouraging sign of ongoing commercial momentum.

In particular, OLG got a shout-out from the CEO. However, his remarks didn’t offer much in the way of hard numbers regarding projected revenue contribution:

“On the 27th of January, we transitioned this full contract with OLG, taking on responsibility for the sportsbook, operating through 2032. We launched with OLG and its PROLINE+ brand both online and across 10,000 retail locations, a major undertaking, and that’s a fantastic achievement by everyone involved.”

Kambi’s agreements with the likes of Coolbet, FDJ UNITED, and Superbet Group, as well as new turnkey sportsbook partnerships, will probably contribute to future growth prospects, as the CEO suggests.

“Since our last report, where we announced Superbet and Coolbet, we’ve added FDJ UNITED and, more recently, ComeOn to the growing list of Odds Feed+ partners. This builds on earlier wins with LeoVegas and Hard Rock, and shows how the product is resonating with Tier 1 operators.

“Yes, there are established incumbents in the Odds Feed+ space, but over time, I’m confident we can grow our share to become a material and meaningful contributor to our business,” said Bacher.

Asked by analysts what share of 2026 revenue the company expected to come from modular products (i.e., interchangeable software or hardware components that allow operators to build, customize, and scale their gaming platforms), the answer from Becher was encouraging for company shareholders. “It’s growing. I would say it should be north of 10% this year, in the 10% to 15% range, I think.”

Becher also referred to a possible tailwind after the recent suspension of the tax introduced in Colombia in Q1 2024:

“The market changed only, I think, three weeks ago when this new tax was suspended. We see already now that customers in Colombia are changing their marketing strategy, their bonus and engagement strategy.

“I think it’s too early to say how this will change market growth for our customers, but of course, we expect some very nice tailwind from this market.”

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.