Entain records H1 NGR of £2.4bn – although HMRC settlement heavily impacts results

Entain has seen its NGR grow 14% year-on-year – while its gross profit stands at £1.46bn.

Key highlights:

– Net debt hits four-year high of £2.59bn

– Entain’s current market capitalisation hits £8.58bn, after a rocky year so far for its share price

– The company’s underlying EBITDA is at a high of £499.4m

– Meanwhile, BetMGM sees an annual growth of 65%

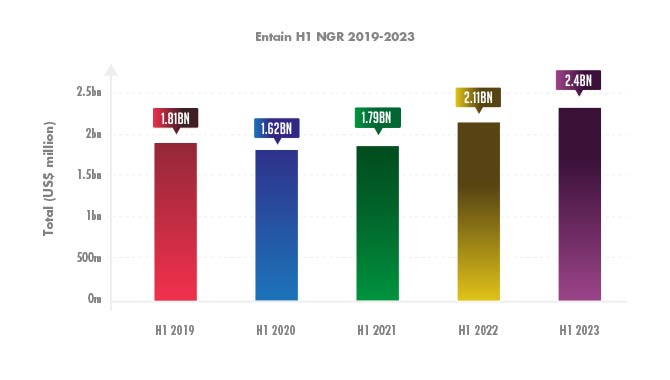

Entain has posted its H1 report for 2023, revealing net gaming revenue (NGR) of £2.4bn ($3.06bn).

The sum represents a 14% increase on H1 2022, where it posted £2.1bn – while its general revenue saw a similar increase, making £2.38bn against H1 2022’s £2.1bn.

Breaking down its NGR, Entain’s online business increased by 15% annually, while retail saw a 12% rise year-on-year – however, its 50% stake in BetMGM gave Entain its biggest percentage increase, reporting 65% growth year-on-year. In total, BetMGM saw an H1 NGR of $944m.

The graph below shows Entain’s NGR since 2019, showing a steady rise since 2020 – before which it saw an 11% drop from 2019 to 2020.

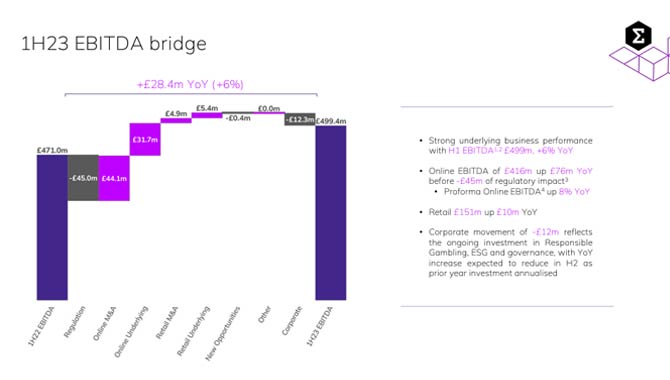

Meanwhile, Entain’s underlying EBITDA increased by 6% from H1 2022, with a figure of £499.4m reported in H1 2023.

Since 2021, Entain’s underlying EBITDA has risen, albeit incrementally – with H1 2021 posting £401.1m and H1 2022 recording £471m.

The graph below (provided by Entain) shows its ‘EBITDA bridge,’ in which it details its £28.4m annual H1 growth.

Source: Entain

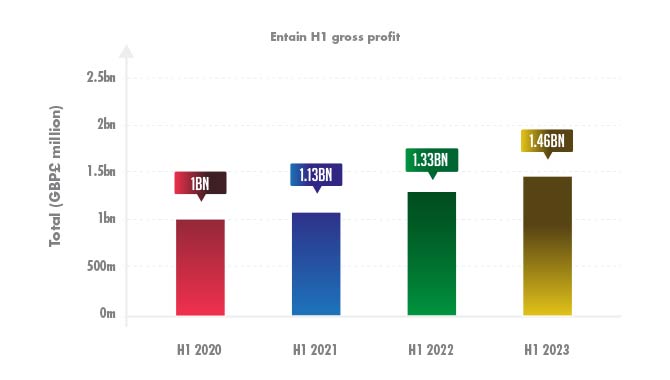

Meanwhile, looking at Entain’s gross profit, which totalled £1.46bn in H1 2023, its 10% increase on H1 2022’s £1.33bn represents smooth growth for the company annually.

Over the course of the last four years, as the graph below shows, Entain’s gross profit has – in a similar fashion to its NGR and underlying EBITDA – risen steadily.

However, despite its gross profit rising, overall for H1 2023, Entain has made a loss of £502.5m, compared to a profit of £28.1m.

The heavy loss is primarily down to Entain putting £585m aside for a settlement in regards to the Crown Prosecution Service’s ongoing investigation into the company’s Turkish operations – which it sold in 2017 under the name of GVC Holdings.

Otherwise, the figures suggest that Entain would have made a profit of circa £82.5m.

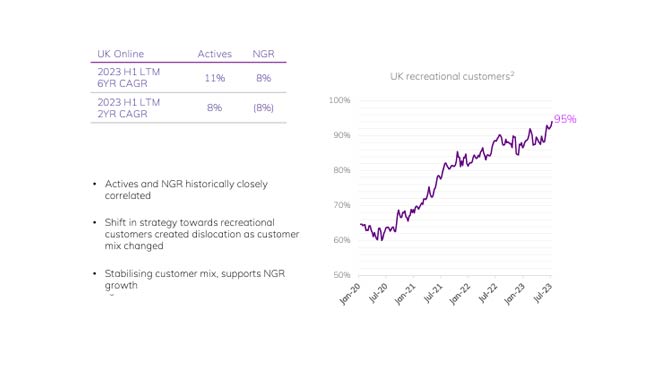

Entain’s own data also reveals that its UK recreational customer base has been growing significantly in the past four years – rising to 95% by July 2023, which can be seen in the graph below.

Source: Entain

Additionally, Entain’s net debt now sits at £2.59bn – higher than it was a year ago when it recorded a £2.21bn figure. Over the course of the previous four years, Entain’s net debt has only fallen below the two-billion threshold once, which came in H1 2021 when it totalled £1.95bn.

Since the start of 2023, Entain’s share price has seen significant rises and falls – with reports of a takeover bid from MGM causing spikes. On January 3, Entain recorded a price of £13.50, with a yearly high of £15.87 coming on February 3 – meanwhile, its yearly low came on March 28, when it fell to £11.71.

its market cap stands at £8.58bn – a price that’s still significantly lower than the $20bn offer tabled by DraftKings for the company in 2021

As of the time of writing, Entain’s price stands at £13.33, while its market capitalisation stands at £8.58bn – a price that’s still significantly lower than the $20bn offer tabled by DraftKings for the company in 2021.

Gambling Insider delivers the latest industry news, in-depth features, and operator reviews that you can trust. Our team combines rigorous editorial standards with decades of specialized expertise to ensure accuracy and fairness. We are committed to delivering clear, impartial, and dependable coverage across the global gambling sector.